Lately, investors’ sentiments have warmed up to Focused Funds that are witnessing net positive inflows at a time when other subcategories of equity mutual funds are struggling.

Does it make sense to invest in Focused Funds at this juncture, especially when the macroeconomic conditions are gloomy?

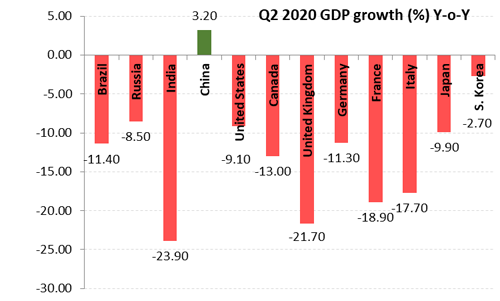

As you may know, India’s Q1FY21 GDP has contracted sharply by -23.9%. Barring agriculture, forestry, and fishing, the other sectors such as manufacturing, services, and defence and public administration have reported sharp contractions.

While the GDP growth contraction was expected due to the COVID-19 pandemic, what is shocking is that it is the worst in over decades and among the BRIC and advanced economies.

Graph: India’s GDP growth shocker

Data as of June 2020 quarter for GDP at constant prices (2011-12 for India)

(Source: www.tradingeconomics.com )

Several agencies have revised their full-year GDP estimates growth estimates for India downwards to around -10% from about -5% projected earlier.

At this rate, a virus-led global recession looks inevitable. Looking at the industry-wise details of India’s GDP growth data, it appears even a V-shaped recovery won’t be enough to push India’s GDP growth in the positive territory for the ensuing few quarters.

Only if we look beyond FY21, due to a favourable base effect, some recovery may be expected from Q3FY22 – provided the COVID-19 pandemic is successfully contained, geopolitical tensions ease, and the year 2021 is less eventful with negativity.

The positive events need to outweigh the negative ones so that market sentiments get a boost, jobs are created, consumers feel confident, and corporate India regains lost ground. These are crucial undercurrents to build wealth.

For now with the second wave of coronavirus, escalating geopolitical tensions, widening fiscal deficit, and India’s sovereign rating at lowest investment grade (with a negative outlook), the negative undercurrents would hold back the upside for the Indian equity market.

In such a scenario then, the question arises:

Can a Focused Fund Reward you (the investor) well?

To answer that, let’s first understand the traits of a Focused Fund.

As per the capital market regulator’s mutual fund categorization and rationalization norms, a Focused Fund is a sub-category of equity-oriented mutual funds that focuses on a maximum of 30 stocks, deploying a minimum 65% of its assets in equity & equity related instruments.

Moreover, the fund also needs to state its focus area, i.e. large-cap, multi-cap, mid-cap or small-cap. That said, most Focused Funds follow a multi-cap approach with a large-cap bias.

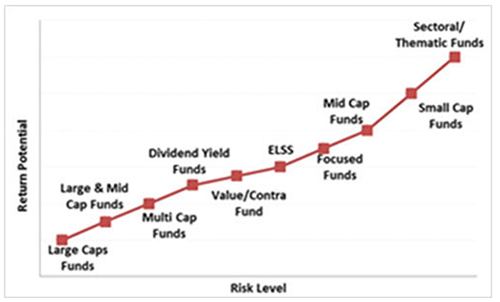

Graph 1: Placement of Focused Funds on the risk-return spectrum

Note: For illustrative purpose only

(Source: PersonalFN Research)

On the risk-return spectrum a Focused Fund, usually, is placed on the higher-end – just below mid-cap and small-cap funds. This is because of the portfolio concentration risk of a Focused Fund.

The fortune of a Focused Fund is hinged on how the conviction bets based on the rationale of the fund manager have performed.

In a broad-based rally (as what we witnessed in the Indian equity market since March 23 low), a Focused Fund usually tends to perform well. On the other hand, if the equity market rally is limited to a few set of stocks, a Focused Fund may not perform well unless it has exposure to such companies.

Here’s how Focused Funds have fared over the last few years…

Table: Report card of Focused Funds

| Scheme Name | AUM (Rs crore) | Absolute (%) | CAGR (%) | Std Dev | Sharpe | ||||

| 6 Months | 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | ||||

| IIFL Focused Equity Fund(G)-Direct Plan | 930 | 2.5 | 13.4 | 7.6 | 8.1 | 13.1 | NA | 23.10 | 0.09 |

| Axis Focused 25 Fund(G)-Direct Plan | 11,372 | 0.4 | 7.8 | 1.4 | 6.8 | 12.6 | 16.4 | 20.71 | 0.07 |

| SBI Focused Equity Fund(G)-Direct Plan | 10,248 | -0.2 | 8.0 | 3.2 | 8.0 | 11.6 | 18.1 | 19.94 | 0.08 |

| IDFC Focused Equity Fund(G)-Direct Plan | 1,400 | 8.8 | 17.4 | -0.2 | 2.8 | 10.6 | 12.6 | 22.09 | 0.01 |

| Principal Focused Multicap Fund(G)-Direct Plan | 393 | 4.5 | 11.0 | 2.6 | 5.3 | 9.4 | 14.1 | 18.74 | 0.04 |

| JM Core 11 Fund(G)-Direct Plan | 49 | -8.4 | -6.4 | -5.1 | -1.7 | 9.3 | 15.6 | 22.95 | -0.03 |

| Motilal Oswal Focused 25 Fund(G)-Direct Plan | 1,265 | 3.7 | 9.1 | 2.7 | 4.0 | 9.2 | 15.4 | 19.96 | 0.02 |

| Sundaram Select Focus(G)-Direct Plan | 1,036 | 3.1 | 2.9 | 0.3 | 5.5 | 9.1 | 12.5 | 19.98 | 0.05 |

| ICICI Pru Focused Equity Fund(G)-Direct Plan | 755 | 16.1 | 7.6 | -1.5 | 5.0 | 8.5 | 12.4 | 18.58 | 0.03 |

| Aditya Birla SL Focused Equity Fund(G)-Direct Plan | 4,115 | 4.1 | 4.2 | 0.0 | 2.5 | 8.3 | 14.3 | 20.48 | 0.01 |

| Quant Focused Fund(G)-Direct Plan | 5 | 14.4 | 7.9 | -0.9 | 2.9 | 8.3 | 17.1 | 21.02 | 0.01 |

| Nippon India Focused Equity Fund(G)-Direct Plan | 3,685 | 7.6 | 5.1 | -2.9 | 0.6 | 7.7 | 18.6 | 25.17 | 0.00 |

| DSP Focus Fund(G)-Direct Plan | 1,769 | 2.2 | 4.4 | -0.6 | 2.1 | 7.1 | 14.2 | 23.03 | 0.01 |

| Franklin India Focused Equity Fund(G)-Direct Plan | 7,106 | -1.6 | -5.7 | -4.1 | 0.6 | 6.0 | 16.2 | 23.57 | 0.00 |

| HDFC Focused 30 Fund(G)-Direct Plan | 499 | 3.4 | -7.0 | -7.3 | -4.0 | 4.0 | 12.1 | 23.58 | -0.06 |

| Category Average | 5.13 | 6.24 | -0.27 | 3.23 | 9.00 | 14.98 | 22.41 | 0.08 | |

| Nifty 500 – TRI | 8.34 | 4.58 | -1.91 | 3.19 | 8.60 | 12.81 | 21.90 | 0.02 | |

Performance data as of September 9, 2020

AUM data as of July 31, 2020

The table above considers only the schemes that have completed 3 years

Point-to-point returns expressed. Returns for periods up to 1 year period are expressed in absolute terms, while those over a year are compounded annualized.

Standard Deviation indicates Total Risk and Sharpe Ratio measures the Risk-Adjusted Return. They are calculated over a 3-Yr period assuming a risk-free rate of 6.25% p.a.

(Source: ACE MF, PersonalFN Research)

On an average, the performance of Focused Funds has been satisfactory across the timeframes. But if you observe carefully, some schemes have miserably underperformed the category average as well the Nifty 500 Total Return Index (TRI) over the last three years. This suggests that you need to be extremely careful while selecting a Focused Fund for your portfolio.

Some of the consistent performers in the category of Focused Funds have been carrying predominantly large-cap portfolios. They have also maintained a blend of defensives and high-betas. And during the ongoing pandemic times, many Focused Funds have increased exposure to IT, Pharma, and Healthcare companies. It is noteworthy that some Focused Funds also appear to engage in frequent portfolio churning; therefore as an investor, you shouldn’t underrate the underlying risk that comes along.

How would Focused Funds fare going forward?

Keep in mind, given the grim macroeconomic condition, volatility is likely to intensify. Currently, the trailing 12-month P/E of the S&P BSE Sensex and the S&P BSE large-cap index is over 28x. The Indian equity is certainly in the expensive zone versus sub-20x levels at the end of March 2020.

When weighed in context with corporate earnings, valuations, particularly in the large-cap segment, appear expensive. In the mid-cap and small-cap segment valuations are lower in comparison to the levels seen in 2017 and 2018, offering a somewhat comfortable margin of safety, albeit very high-risk. If the bellwether index tumbles downs, the mid-and small-cap may also not be spared –may fall even more severely than large-caps.

A point of caution is that India Inc.’s corporate earnings have been significantly impacted by the COVID-19 pandemic. The future is extremely uncertain. How many businesses will survive out this COVID-19 crisis is tough to foretell. FY21 earnings are expected to lag, while some improvement may be expected in FY22. That said, if COVID-19 cases fail to recede, geopolitical tensions escalate, and macroeconomic indicators worsen, it would weigh on corporate earnings and the performance of equity as an asset class. For equities to move up ultimately, earnings need to justify valuations; otherwise, markets may slip back – particularly when liquidity begins to dry up.

In the above scenario, if the portfolio characteristics of a Focused Fund are not worthy, conviction bets do not pay off; clocking high returns could be a challenge. Therefore, set realistic risk-return expectations; do not get swayed by past returns.

Here’s how you should NOT pick a Focused Fund:

- Overemphasizing on the past performance

- Taking a short term view on the markets

- Without paying close attention to your overall asset allocation

- Without evaluating a fund on qualitative and quantitative parameters

- By relying excessively on the ability of star fund

- Relying on star ratings and the popularity of funds managers

The trends in the Assets Under Management (AUM) suggest that investors have trusted only popular schemes, as evident from the fact that 5 schemes account for nearly 70% of the category AUM.

To conclude…

Be very careful when you select a Focused Fund for your mutual fund portfolio. Consider adding a Focused Fund only if you have the stomach for high risk and an investment time horizon of at least 5 years. Avoid the New Fund Offers (NFOs) of Focused Funds.

This article first appeared on PersonalFN here

{kind=link}