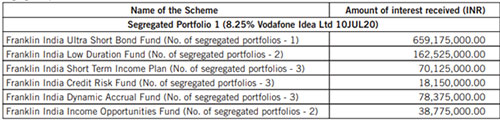

Franklin Templeton Mutual Fund (FTMF) received interest payment from Vodafone-Idea bonds on June 12, 2020, held in the segregated portfolio of its debt schemes. The amount received was for 8.25% Vodafone Idea Ltd bond which matures on July 10, 2020.

The six schemes of FT that were wound-up had exposure to the said paper of Vodafone-Idea (VIL) in its segregated portfolio. FT has processed the payment to be distributed to the investors in the scheme in the proportion of their holdings. After the payment, the number of units outstanding in the investor account under said segregated portfolio of the scheme would fall to the extent of payout and statutory levy (if applicable).

According to a statement from FT, “The Record Date for the units held in demat mode will be June 19, 2020. For units held in physical/ Statement of Account mode the holding as on June 12, 2020 shall be considered for processing these transactions. All the Unitholders / Beneficial Owners of the segregated portfolio of the scheme under various Plans/options whose names appear in the records of Registrar / Depositories as on the relevant date shall be entitled to receive recovery proceeds.”

Table 1: FT receives partial payment under segregated portfolio

(Source: Franklin Templeton Mutual Fund)

Apart from 8.25% Vodafone-Idea 10-Jul-2020, the segregated portfolios of the schemes have exposure to 10.90% Vodafone Idea Ltd 02-Sep-2023(P/C 03-Sep-2021) and 9.50% Yes Bank Ltd CO 23-Dec-21.

FT had one of the highest exposures among mutual funds to debt of VIL. Post Supreme Court’s Verdict on AGR dues in January, FT immediately marked down its entire exposure in debt securities of VIL and later created a side-pocket for the exposure.

Though the amount investors receive from VIL interest payment will be marginal, it could be seen as a positive sign regarding future payments from the telco. Sizeable payments can be expected once FT begins monetization of the main portfolio.

Notably, no payout has been made yet from the main portfolio of the wound-up schemes. It can be only done after successful completion of the voting process and when all the schemes turn cash positive. Till now only two of the wound-up schemes viz. FIUBF and FIDA have turned cash positive (have repaid borrowings).

FT had to suspend the voting process scheduled between June 09 and June 11 after Gujarat High Court’s stay order.

Alongside, an investor group in Chennai has moved to court seeking to safeguard nearly Rs 28,000 crore of investors’ money stuck in the wound-up schemes, while there is another petition in Delhi Court challenging the winding-up of six schemes.

Subsequently, Franklin Templeton moved the Supreme Court to vacate the stay order. SEBI has also filed a ‘patent appeal’ against the Gujarat High Court order staying the entire e-voting process of winding up of the debt schemes.

During the hearing which was held today, SC refused to intervene in the matter as the case is still being heard in the lower courts. It has decided to transfer all the ongoing cases against the AMC to Karnataka High Court. The Gujarat High Court also adjourned the appeal filed by SEBI.

Legal proceedings could further delay the distribution of money to investors.

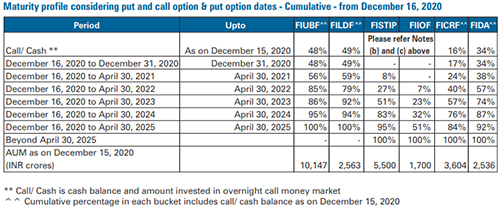

Table 2: Expected timeline of payout from wound-up schemes of FTMF

(Source: Franklin Templeton Mutual Fund)

Thus for investors in the schemes, the battle for recovery of their money could be long drawn.

[Read: Franklin Templeton Fiasco: Here Is When You Can Expect to Get the Money Back]

Even if one assumes all the legal matters at hand will resolve soon, very few schemes are expected to liquidate a significant part of the portfolio in the next 2-3 years.

As seen in the table above investors in Franklin India Ultra Short Bond Fund (FIUBF) and Franklin India Low Duration Fund (FILDF) will be able to recover a substantial sum in the next 2-3 years. Investors in Franklin India Short Term Income Fund (FISTIP), Franklin India Credit Risk Fund (FICRF), and Franklin India Dynamic Accrual Fund (FIDA) will receive a major chunk only after 3-4 years.

The wait will be longest for investors in Franklin India Income Opportunities Fund (FIIOF). The scheme is expected to liquidate just around 55% of the portfolio in the next five years, while other schemes may be able to liquidate anywhere around 84-100% of the assets during the same period.

The only way for faster payouts is if FT starts receiving prepayments or accelerated payments by the issuer companies and by selling securities in the secondary market.

However, the current market scenario is rife with risk aversion and illiquidity. The fact that wound up schemes have high holdings of lower rated securities, FTMF will have to wait for the market conditions to go back to normal to liquidate the portfolio at the earliest, without causing value erosion for investors.

The way ahead…

While the fund house has done this to protect investors’ interest, it has made the funds illiquid from the investors’ point of view. Many investors may lose faith in debt funds as preferred investment avenues for their financial goals.

[Read: Lessons Learnt from the Debt Fund Crisis]

[Also Read: Who Is to Blame for the Franklin Templeton Fiasco?]

It is time for the regulator to step up and provide a framework of strict guidelines to restrict fund managers from putting investors’ hard-earned money at risk by exposing them to low rated securities for potentially higher yield.

This article first appeared on PersonalFN here

{kind=link}