A recent survey of nearly 1,330 people conducted by Nielsen India across 23 Indian cities paints a gloomy picture for the companies dependent on consumer spending in the post-COVID-19 world. Approximately 64% of the respondents expressed that they would spend less on restaurant and movie visits, while 54% indicated that spending on automobiles, luxury brands, and leisure travel would become less important to them in an adversely changing economic environment. And, nearly 43% said they were likely to cut their lifestyle expenditure.

Have Indians suddenly become parsimonious during the COVID-19 lockdowns?

Is the great Indian consumption story beginning to wane?

A fact is, barring companies that sell essential goods like food articles and other small-ticket discretionary items, other companies in the ‘Consumer Durable’ segment viz. car and two-wheeler manufacturers, certain home appliance manufactures (particularly TV, Refrigerators, and Air-Conditioners) are now feeling the heat.

In the present environment of job losses, pay cuts, deferred payment due to the COVID-19 crisis, for most consumers, affordability is an important consideration in the buying decisions and risk-aversion has set in. Most people are conserving cash — perhaps anticipating that things might worsen in time to come.

That being said, calling the downtrend in consumption a dead-end, would be a mistake! After all, India is a young country with an insatiable appetite backed by aspirations and has a long way to go.

When normalcy returns (which will take a year or more and provided we do not witness a second wave of coronavirus and/or any other catastrophic event), people will be back to consuming discretionary goods. Currently, only about 22 people out of 1,000 own a car in India, and the penetration of air-conditioners is a little under 10%.

Taking near and dear ones out for a movie or dinner is although discretionary, most of us do endeavour to spend time with near and dear ones, unwind, and enjoy a good life. For this reason, many of the restaurant and entertainment businesses have sustained. In a post-COVID-19 world, the recovery is likely to be slow but writing off the consumption themes would be incorrect.

All factors considered, India’s consumption story is here to stay!

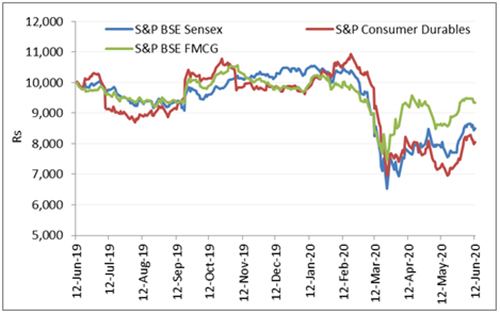

Graph 1: How have FMCG and Consumer Durable Companies fared?

Data as of June 12, 2020

Base Rs 10,000 taken for the respective indices.

(Source: bseindia.com, PersonalFN Research)

The data reveals that consumption-oriented stocks, particularly the Fast Moving Consumer Goods (FMCG) companies, have done relatively well not only during the COVID-19 lockdown but even before — when the economic growth began to dwindle.

The point to note is that, be it a slowdown or recession, people do not stop buying or consuming the things they truly need. Salt, flour, rice, tea, coffee, biscuits, certain processed food products, toothpaste, soaps, detergents, etc. are necessities and people do not wait to buy them. This is unlike discretionary goods such as a two-wheeler, a car, a TV, AC, etc., which can be pushed to another day. So, FMCG (like pharma) is a defensive sector.

Rs 10,000 invested in the S&P BSE FMCG Index on June 12, 2019, is of course down to Rs 9,342 as of June 12, 2020, but has fared better than the S&P Consumer Durables and the S&P BSE Sensex.

Table 1: Report card of Consumption-oriented Mutual Funds

| Category Average | Returns (Absolute %) | Returns (CAGR %) | |||

| 6 Months | 1 Year | 3 Years | 5 Years | 7 Years | |

| BNP Paribas India Consumption Fund | -5.2 | 3.1 | – | – | – |

| Nippon India Consumption Fund | -5.4 | -1.9 | 0.0 | 6.9 | 9.4 |

| UTI India Consumer Fund | -8.1 | -3.1 | 2.0 | 5.4 | 9.2 |

| ICICI Pru FMCG Fund | -6.6 | -4.4 | 5.2 | 9.7 | 11.2 |

| Tata India Consumer Fund | -7.1 | -4.5 | 5.3 | – | – |

| ICICI Pru Bharat Consumption Fund | -9.5 | -6.0 | – | – | – |

| Quant Consumption Fund | -3.0 | -6.6 | -1.3 | 8.1 | 14.6 |

| Mirae Asset Great Consumer Fund | -14.4 | -8.8 | 4.9 | 9.2 | 15.1 |

| Mahindra Manulife Rural Bharat and Consumption Yojana | -12.1 | -13.0 | – | – | – |

| SBI Consumption Opp Fund | -17.8 | -16.5 | -0.4 | 7.4 | 9.3 |

| ICICI Pru Commodities Fund | -10.8 | – | – | – | |

| NIFTY CONSUMPTION – TRI | -4.2 | -2.7 | 3.6 | 8.3 | 11.7 |

Data as of June 12, 2020

(Source: ACE MF, PersonalFN Research)

Over the last 1 year, the performance of Consumption-oriented Funds in India is nothing to vie for; on the contrary, investors’ wealth is eroded.

But over longer periods, i.e. 5 years and 7 years certain schemes, such as ICICI Pru FMCG Fund, Mirae Asset Great Consumer Fund, and SBI Consumer Opportunities Fund have delivered respectable returns. Over a 5-year time frame, the consumption-oriented funds have outperformed all other sub-categories of diversified equity mutual funds (see Table 2), plus consistently outperformed the broader markets.

Table 2: Consumption funds have outperformed other sub-category of diversified equity funds

| Category Average | Returns (Absolute %) | Returns (CAGR %) | |||

| 6 Months | 1 Year | 3 Years | 5 Years | 7 Years | |

| Consumption Funds | -8.8 | -6.2 | 1.8 | 7.5 | 11.5 |

| Mid Cap Funds | -10.1 | -10.1 | -1.5 | 5.6 | 14.9 |

| Focused Funds | -13.1 | -10.6 | 1.5 | 6.8 | 12.7 |

| Dividend Yield Funds | -10.2 | -11.0 | -1.7 | 4.6 | 9.6 |

| Large & Mid Cap Funds | -13.8 | -12.0 | -0.4 | 6.2 | 13.0 |

| Multi Cap Funds | -13.7 | -12.0 | 0.3 | 5.7 | 12.2 |

| Large Cap Funds | -14.6 | -12.5 | 1.2 | 5.8 | 10.9 |

| Contra Funds | -12.8 | -14.0 | 0.9 | 6.3 | 12.1 |

| Small cap Funds | -11.9 | -16.4 | -6.3 | 4.2 | 13.6 |

| Value Funds | -15.1 | -17.5 | -3.9 | 4.5 | 12.0 |

| NIFTY CONSUMPTION – TRI | -4.2 | -2.7 | 3.6 | 8.3 | 11.7 |

| S&P BSE 500 – TRI | -14.9 | -14.6 | 0.5 | 5.9 | 10.3 |

| NIFTY 200 – TRI | -15.3 | -14.6 | 1.2 | 5.9 | 10.1 |

Data as of June 12, 2020

(Source: ACE MF, PersonalFN Research)

So, where are Consumption Funds investing?

Over the last two months, consumption-oriented funds did some cherry-picking in beaten-down sectors such as leading FMCG companies, hotels, increased weightage to telecom, and insurance companies. However, they reduced exposure to companies deriving revenues predominantly from leisure businesses.

In comparison, the portfolio traits of diversified funds have been more consistent and driven largely by stock-specific activities in most cases not just the sectoral trends …and hence more diversified.

Being sector and thematic, Consumption Funds have a narrow choice for stock selection while usually following a top-down approach. On the other hand, diversified equity mutual funds go by broader macroeconomic trends and not necessarily one sector or theme. Thus, they tend to do well during economic and market upswings.

In case you are unaware, FMCG was one of the worst-performing sectors during the upswing of 2003-08. So, even if you were to bet on the consumption theme, it would be unwise to go overboard. It can have its bouts of underperformance in times of exuberance.

Especially when valuations appear overbearing in the consumption theme, betting unreasonably on the consumption theme will prove imprudent. Only around 10% of the entire equity mutual fund portfolio may be parked in Consumption-oriented Funds, provided you have optimally built a strategic portfolio of diversified equity funds.

I would like to share with you a secret strategy of creating a strategic portfolio of diversified equity funds, based on the ‘Core & Satellite’ approach to investing. This is a time-tested investment strategy followed by some of the most successful investors to build a portfolio.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions. Plus, the ‘Satellite’ portfolio provides the opportunity to support the ‘Core’ by taking active calls based on extensive research.

The ‘Core’ holding should comprise around 65-70% of your equity mutual fund portfolio and consist of large-cap fund, multi-cap fund, and a value style fund. Whereas, the ‘Satellite’ holdings of the portfolio can be around 30-35% comprising of a mid-cap fund, a large & mid-cap fund, and an aggressive hybrid fund.

To build a strategic portfolio of mutual funds, here are a few set of rules:

- The selected mutual fund schemes should be amongst the top scorers in their respective categories. The portfolio should be built with a time horizon of at least five years.

- It should be diversified across investment styles and fund management.

- Each mutual fund scheme should be true to its investment style and mandate.

- The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place.

- Each fund should have seen outperformance over at least three market cycles

- The portfolio should contain an adequate number of schemes in the right proportion. In short, it should carry the most optimum allocation to each scheme and investment style.

- The number of schemes in your portfolio must be limited to seven.

- Not more than five mutual fund schemes should be managed by the same fund manager.

- Not more than two mutual fund schemes from the same fund house should be included in the portfolio.

The advantages of following the ‘Core & Satellite’ approach are:

- Facilitates optimal diversification

- Reduces the need for constant churning of your entire portfolio

- Reduces the risk to your portfolio

- Enables you to benefit from a variety of investment strategies

- Aims to create wealth cushioning the downside

- Holds the potential to outperform the market

Given the uncertainty looming, and the Indian equity market would remain very volatile until normalcy returns’, prefer Systematic Investment Plan (SIP) route while you build the portfolio the equity mutual fund portfolio the ‘Core and Satellite’ way and don’t forget to align your investments with your risk appetite, broader investment objective, financial goals, and time horizon to accomplish the envisioned financial goals.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}