The entire world is in damage-saving mode. Coronavirus or COVID-19 pandemic has turned the world upside down. At the beginning of the year 2020, nobody would have thought that we were going to face such a catastrophic event just within a few weeks. India reported its first COVID-19 case on January 30th 2020, and since then the number of confirmed COVID-19 cases are on the rise.

Newsrooms are buzzing with stories around COVID-19. Indeed COVID-19 has taken centre stage and it is detrimentally playing out on equity markets as well. Since the all-time high of the S&P BSE Sensex of 42,273.87 points (made on January 20, 2020), we have nosedived nearly 30%. Even the mid-cap and small-cap have noticeably fallen since their peaks in January 2018. As a result, the mutual fund NAVs too have taken a hit and portfolios are bleeding amid the COVID-19 pandemic.

Table: COVID-19 infecting equity mutual funds…

| Category | 30/Jan/20 To 03/Apr/20 (%) | 1 Year (%) | 3 Years (%) | 5 Years (%) |

| Aggressive Hybrid Fund | -23.7 | -20.0 | -2.7 | 1.6 |

| Contra Funds | -32.1 | -29.6 | -4.3 | 0.5 |

| Dividend Yield Funds | -28.3 | -25.8 | -6.0 | 0.0 |

| Equity Savings Funds | -13.1 | -9.2 | 0.9 | 4.1 |

| Focused Fund Funds | -30.4 | -24.4 | -3.1 | 1.7 |

| Market Cap Fund Funds | -31.4 | -26.4 | -5.2 | 0.6 |

| Value Funds | -33.6 | -33.1 | -9.0 | -1.0 |

| NIFTY 50 – TRI | -32.6 | -29.6 | -3.1 | 0.1 |

| NIFTY 500 – TRI | -32.8 | -30.3 | -5.0 | 0.0 |

Data as on April 3, 2020

Return upto 1-year is absolute, while the return for the periods over 1 year is compounded annualized.

(Source: ACE MF, PersonalFN Research)

How have you been handling this stressful situation and ensuring that your clients don’t get a rough deal in the on-going bear market phase?

Are you protecting your investors mutual fund portfolios?

And don’t misread the above questions. Protection does not mean simply to avert negative returns; it actually means not letting investors’ portfolio lose disproportionately. Protecting portfolios means ensuring the damage is measured and well-contained.

Losses are inevitable when markets fall so sharply and enter a serious bear phase. But that does not mean you should sit back and relax until bulls make a comeback. On the contrary, financial advisors should ensure that the investors’ mutual fund portfolios remain well aligned with their financial objectives.

Discourage clients from discontinuing their SIPs

Financial advisors must counsel investors more seriously and take extra effort to explain to them why they would do better if they continue with their SIPs.

Disappointing returns even on 3-year and 5-year time frame might have had investors worried about the future performance of their SIPs. But historical evidence suggests that over the long-term, SIPs in equity mutual funds have generated a respectable compounded annualized return. In other words, the impact of sudden market falls gradually reduces provided investors continue with SIPs. This is because of the inherent rupee-cost averaging feature of SIPs.

As a financial advisor, explain the benefits of doing SIPs one more time; even though you might have explained this information to them at the time of recommending SIPs. Sometimes reiteration of advice is important to mollify and educate investors.

If investors hold unrealistic return expectations, especially during steep downturns like the one prevailing at present, counsel them appropriately. This might take away unnecessary pressure that you might otherwise feel.

That said, don’t forget to revisit investors’ portfolio just to ensure everything is under control.

You should review the portfolios of your clients now as it helps to:

- Identify underperforming schemes and fan them out

- Find suitable alternative mutual fund schemes backed by thorough research

- Facilitate portfolio consolidation

- Attain optimal portfolio diversification

- Makes sure that the portfolio is in sync with investor’s financial objectives, risk appetite and time horizon

Needless to say, do not go overboard in the portfolio review exercise by replacing each and every scheme that has underperformed in the recent market meltdown. You may ignore underperformance due to short-term turbulence or volatility in the market, or possibly because the fund manager took a contrarian bet to the market. It may take some time for the fund to overcome the volatility and the fund manager’s strategy to pay off. Only when repeated underperformance across time periods continues, it suggests that the quality of management is questionable and hence portfolio rejig is warranted.

Below are some signs that a mutual fund scheme is poorly managed:

- Poor characteristics of the portfolio;

- Lack of efficient investment processes & systems;

- Lack of a robust risk management system;

- Poor skills and experience of the fund manager or maybe he/she is overloaded with many schemes

Here’s how the online portfolio review tool on the CFG can help financial advisors review the portfolio of their clients/investors…

First, Log on to www.certifiedfinancialguardian.com and login with your user id and password.

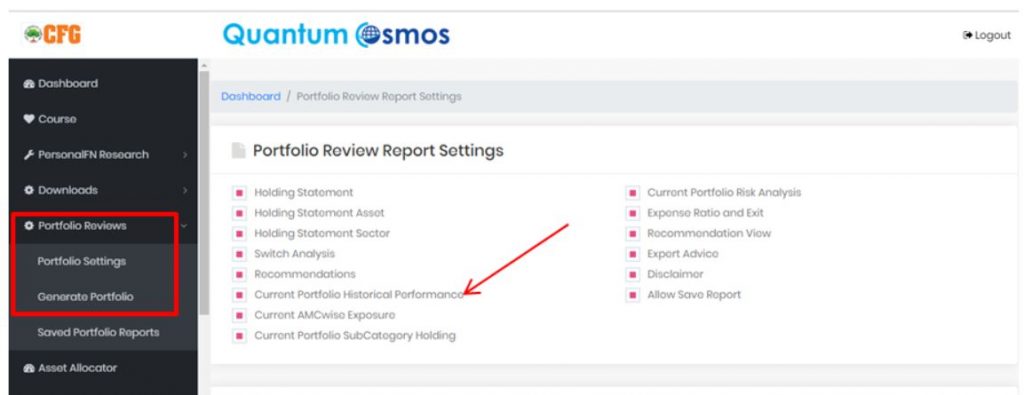

Thereafter, you will come to your dashboard. On the dashboard, click on the Portfolio Review section. You have three drop-down options there: Portfolio Settings; Generate Portfolio; and access to Saved Portfolios Review Reports. Before you generate a portfolio review, you can fine-tune your portfolio settings as per what you would like to include in the Portfolio Review. (see snapshot below).

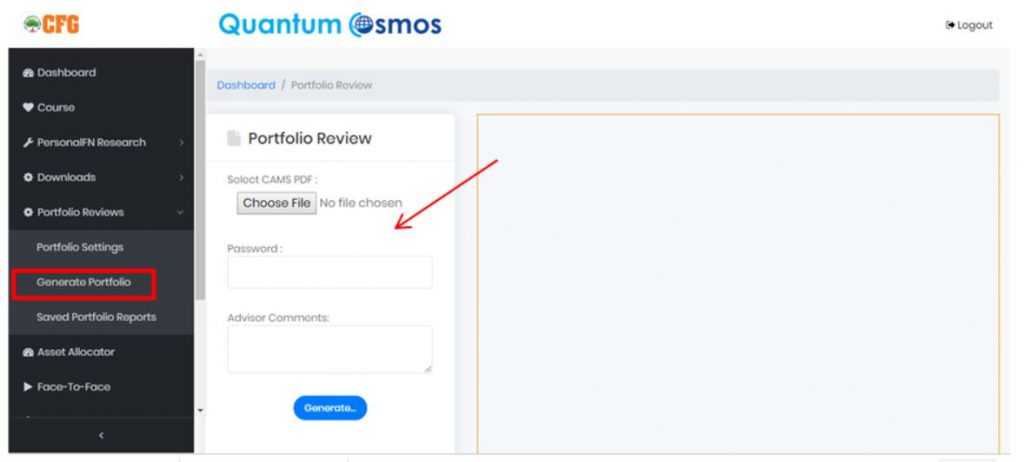

Once you are done with the settings, click on the second option under Portfolio Review i.e., ‘Generate Portfolio’. Once you click on this option, you will be guided to the screen below.

You can choose a client’s portfolio file from desktop, laptop, tablet etc. add your comments, enter the password, click on generate and the system will do a portfolio review seamlessly and efficiently, as per the portfolio review settings you selected and the statement of holdings.

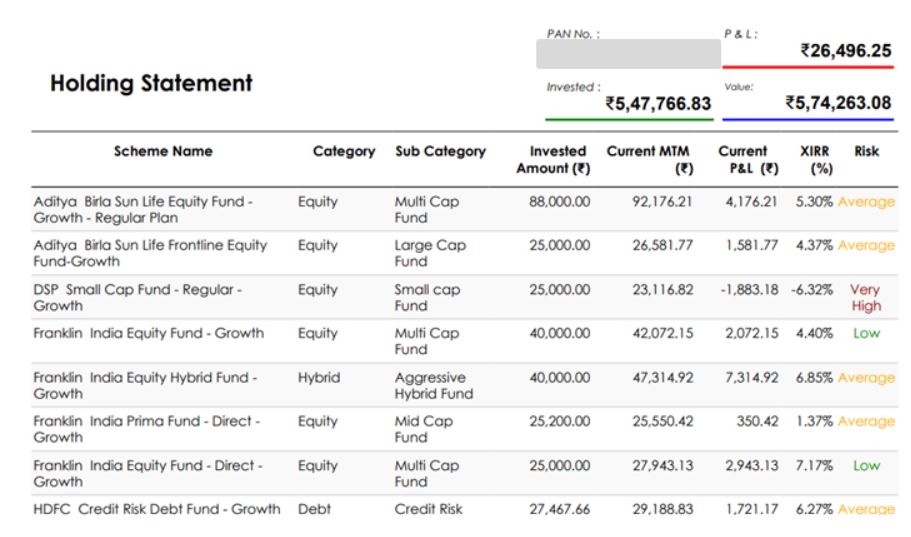

Thereafter, as per the NAV of the holdings, a profit & loss statement will be generated highlighting the CAGR/XIRR or absolute returns generated by the scheme/s, as the case may be, even highlighting the risk traits of every scheme in the portfolio (see snapshot below).

(For illustrative purpose only)

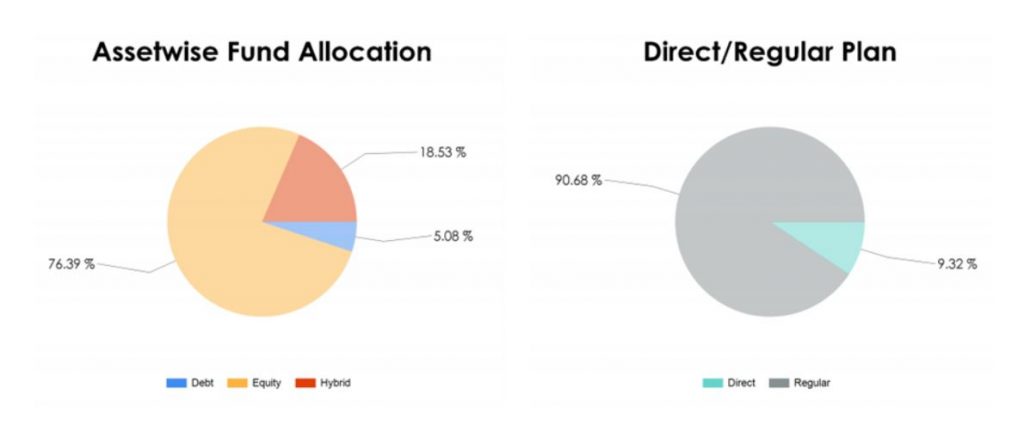

The Portfolio Review will also include an asset-wise allocation to funds––equity, debt, hybrid, etc. ––as well as help you know whether the client’s hard-earned money is parked in the Direct Plan or Regular Plan. If you, as a financial advisor, are of the view that the personalised asset allocation of your client warrants a change due to change in his/her financial circumstance, risk profile, investment objectives, and financial goals along with time horizon for the goals to realise, then you may advise him/her accordingly.

(For illustrative purpose only)

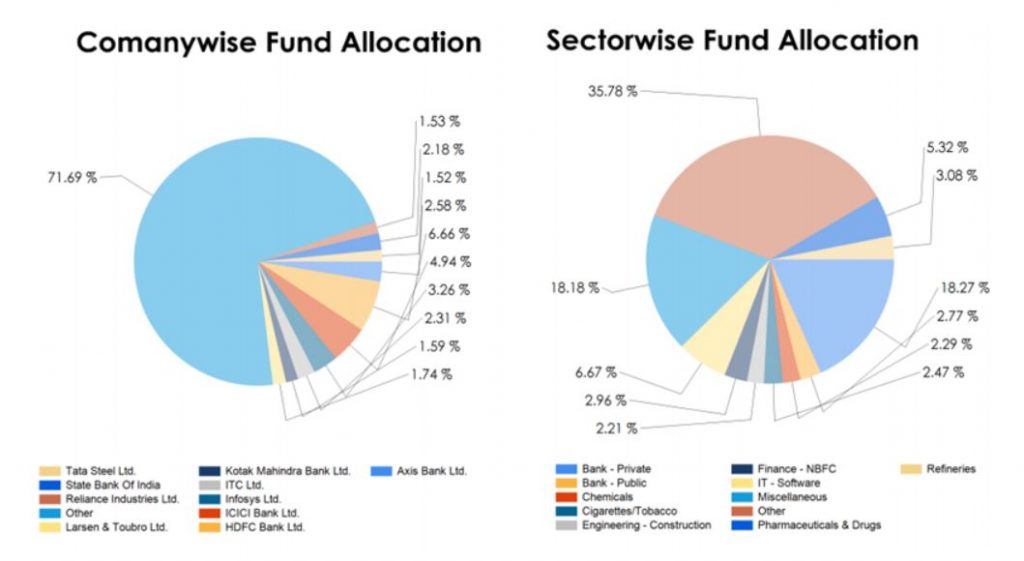

In addition to the above, the Portfolio Review report will also throw light on the company-wise and sector-wise allocation of your client’s money parked in respective mutual fund schemes (see snapshot below). This will help you update the client better on the reasons of outperformance or underperformance, as the case may, recognising the portfolio characteristics of the schemes held.

(For illustrative purpose only)

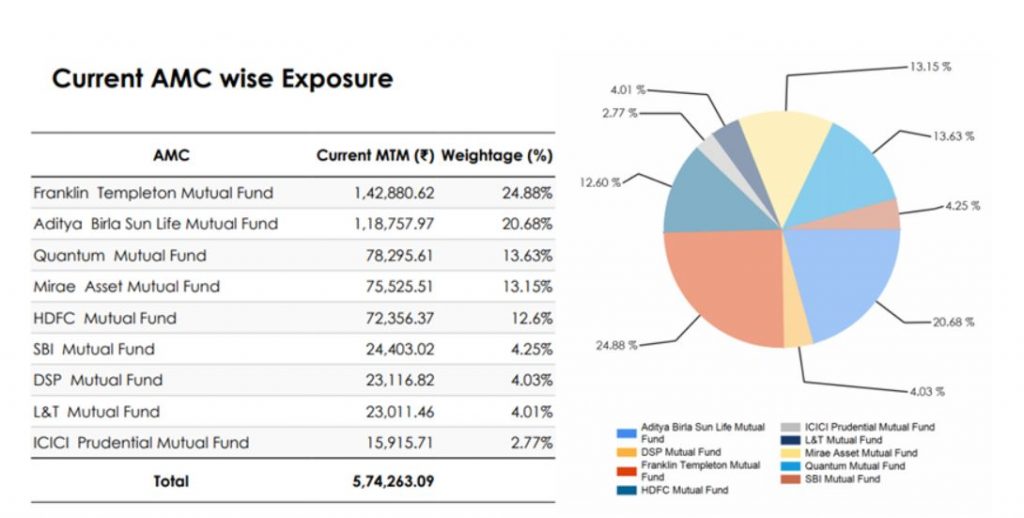

The Portfolio Review will also assess the fund house or AMC wise exposure of a client’s portfolio (see snapshot below) to make sure it is well-diversified across fund houses and to reduce AMC concentration risk. Do note that holding schemes of fund houses with larger Assets under Management (AUM) does not make the mutual portfolio robust or safe. It is not necessary that all schemes of large fund house will prove to be well-rewarding.

(For illustrative purpose only)

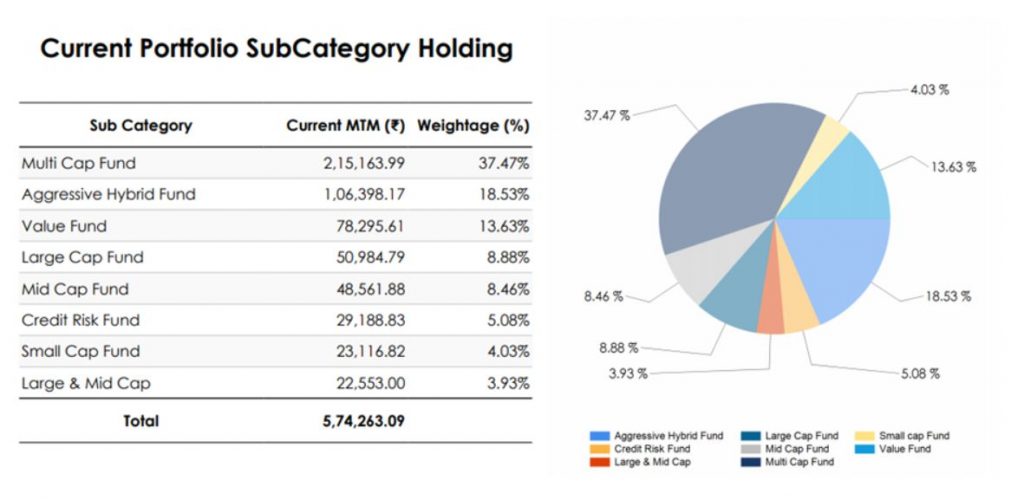

Further, within the category of schemes a client is invested in, a Portfolio Review will shed light on the exposure to various sub-categories of schemes large-cap, multi-cap, value style funds, etc. (see snapshot below).

(For illustrative purpose only)

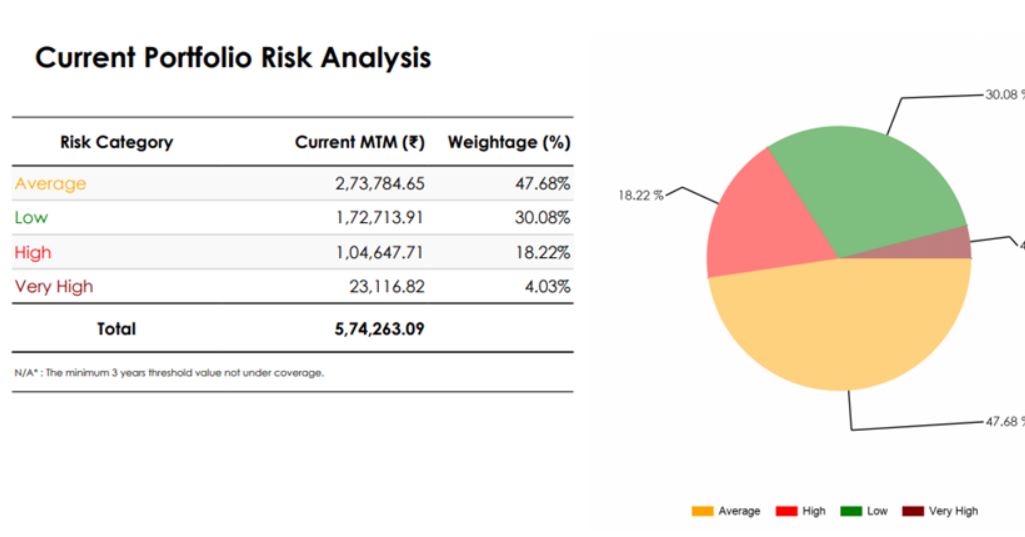

The Portfolio Review will look after the risk analysis of the entire portfolio (see snapshot below). This will help you assess if the schemes held in your client’s portfolio are or not in congruence to his/her risk profile and take timely action.

(For illustrative purpose only)

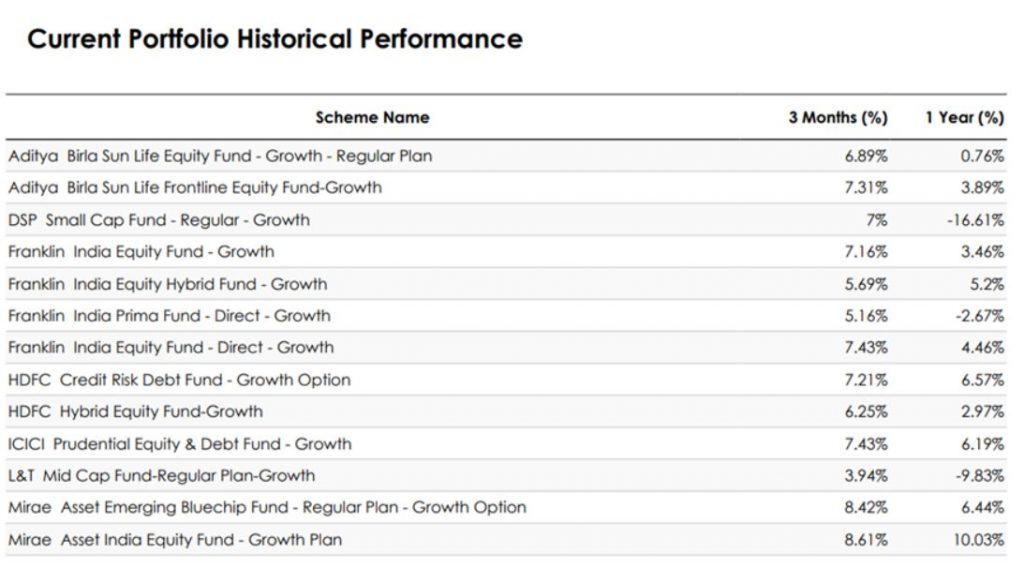

The Portfolio Review report will help you, the financial advisor, and your client to evaluate the historical performance of his/her current mutual fund portfolio (see snapshot below).

(For illustrative purpose only)

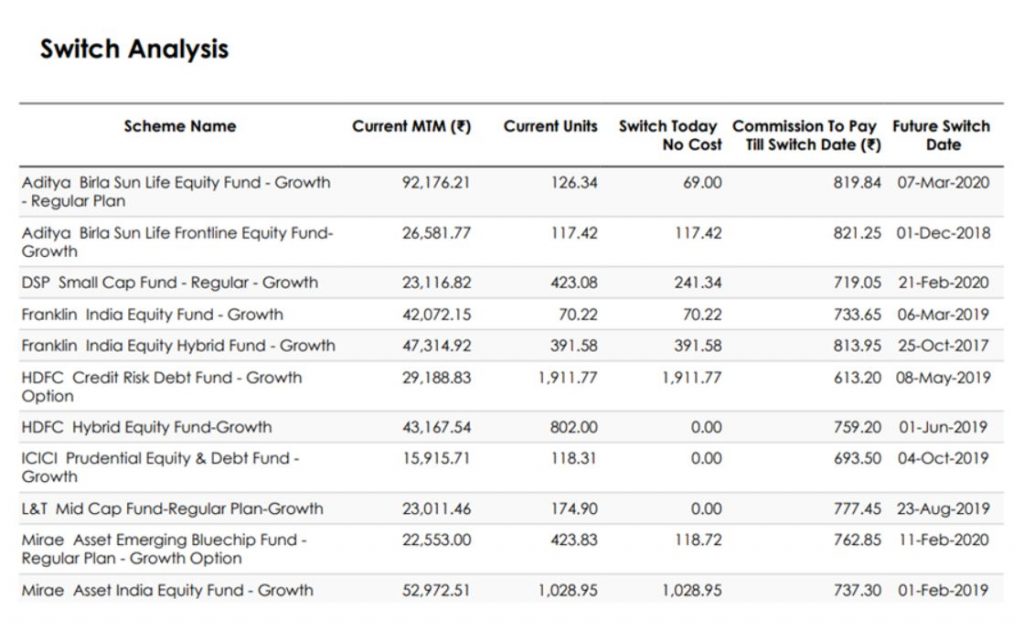

Then, in case if there are any switches – STP, SWPs, etc. a switch analysis too will be performed helping you recognise the cost of switching, the commission to be paid till the date of switch, future switch date and many more details (see snapshot below).

(For illustrative purpose only)

The Portfolio Review will even help assess the expense ratio and exit load implications (see snapshot below).

(For illustrative purpose only)

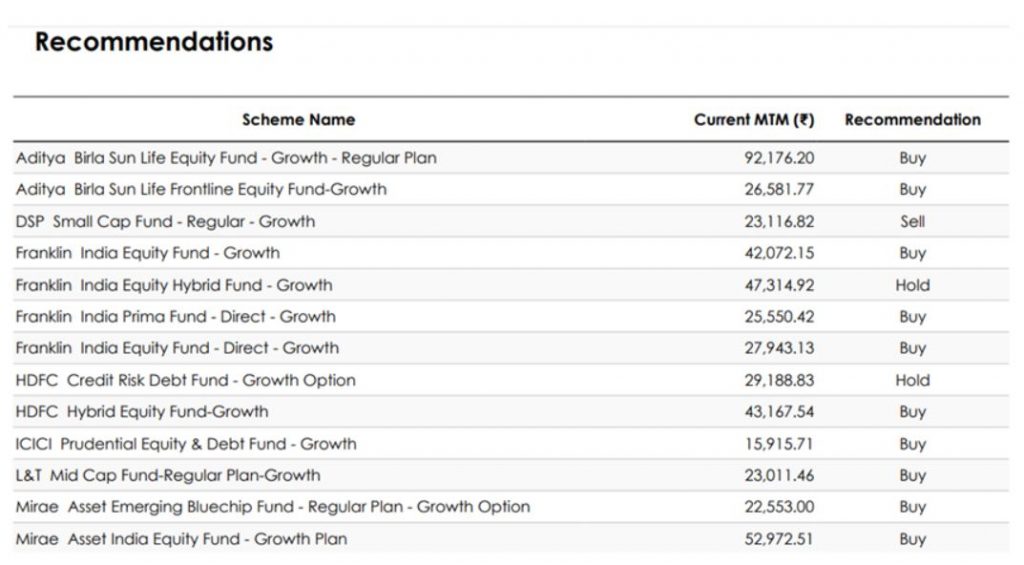

Finally, the Portfolio Reviewer will provide recommendations—Buy, Hold, or Sell—along with the rationale behind it.

(For illustrative purpose only)

So, guide your clients to do a comprehensive Portfolio Review in the COVID-19 pandemic before they take ad-hoc investment decisions that may not be in the best interest of their financial wellbeing.

Endnote…

An unhealthy portfolio not just hinders fulfilling the envisioned financial goals of your valuable clients, but may even jeopardise their wellbeing.

Hence, serve investors/clients, empathetically, ethically, transparently, proficiently, and hand-hold them in the journey of wealth creation, especially during these turbulent times.

Investors/clients look up to you as their ‘financial guardian’ who prudently guides and handle their money with enough care and prudence (much as you would while managing your own hard-earned money). When service is offered diligently, it will earn you the goodwill and help grow your financial advisory business successfully.

{kind=link}