Ever since the debt fund fiascos, investors have become cautious about where they put their hard-earned money. As many liquid funds posted steep losses as they were having exposure to the default companies. It made the investors aware that debt fund investment isn’t completely risk-free.

While liquid funds were widely perceived to be a safe and better alternative to short-term deposits offered by banks, their popularity waned in recent times.

Plus, in March 2019, the regulator notified about valuation norms of money market and debt securities. This made a leeway to launch debt funds that would be more liquid and offers an opportunity to park money for short term requirements in an array of debt and money market instruments having maturity between 3 to 6 months.

Hence even HSBC Mutual Fund launched an open-ended debt scheme, HSBC Ultra Short Duration Fund (HUSDF) that will be investing in instruments such that the Macaulay Duration of the portfolio is between 3 months to 6 months.

What is an ultra-short duration fund?

Ultra-short-term funds invest primarily in debt and money market instruments such that the Macaulay duration of the portfolio is between 3 months to 6 months. Compared to a liquid fund, an ultra-short-term fund invests in higher maturity debt papers and money market instruments.

Note that the bond prices are inversely related to the interest rates. Hence, a bond that has a longer maturity is extremely price-sensitive to changes in the interest rate as compared to bonds having a short duration. An ultra-short-term fund help investor reduces this interest rate risks and offers better returns than most money market instruments.

The Macaulay duration measures the weighted average term to maturity of the bond’s cash flow. The weights in this weighted average are the present value of each cash flow as a per cent of the present value of all the bond’s cash flows.

Macaulay’s Duration is linked to the price volatility of a bond. Duration is the fund manager’s tool for structuring a portfolio of bonds to have the desired sensitivity to maintain between the time interval of invested bonds. As per the mandate, HUSDF will allocate all its assets in derivatives, securitised debts, and in repo within the prescribed limits.

From the risk-return standpoint, HUSDF is a relatively moderately low risk-return. If you are planning for short-term goals, to where the money is required in 3 to 6 months, the ultra-short-term fund may be considered. The ideal time horizon to park money in an ultra-short-term fund is 3 to 6 months.

Graph: Indicative Risk Return Matrix of Fixed Income Funds

^^General strategy followed by the fund categories. Above list is not exhaustive and for illustration purpose only

* Typical duration / maturity period of the investment securities where fund invests

$Overnight Fund redemption -the fund endeavours to make the pay-out within one business day on redemption.

1An open ended debt scheme investing in instruments with Macaulay duration between 4 to 7 years

2An open ended debt scheme investing in government securities across maturity

3An open-ended short-term debt scheme investing in instruments with Macaulay duration between 1 year and 3 years

4Short-term debt scheme investing in instruments with Macaulay duration between 3 months and 6 months

5An open ended low duration debt scheme investing in instruments with Macaulay duration between 6 months and 12 months

(Source: HSBC Ultra Short Duration Fund Product deck)

Table 1: HSBC Ultra Short Duration Fund Details

| Type | An open-ended ultra-short-term debt scheme investing in instruments such that the Macaulay duration of the portfolio is between 3 months to 6 months. | Category | Ultra-Short Duration Fund |

| Investment Objective | To provide liquidity and generate reasonable returns with low volatility through investment in a portfolio comprising of debt & money market instruments. However, there is no assurance that the investment objective of the scheme will be achieved. | ||

| Min. Investment | Rs 5,000 and in multiples of Re 1 thereafter | Face Value | Rs 10 per unit |

| Plans |

| Options |

|

| Entry Load | Not Applicable | Exit Load | Nil |

| Fund Manager | Mr Kapil Punjabi | Benchmark Index | CRISIL Ultra Short Term Debt Index |

| Issue Opens | January 14, 2020 | Issue Closes: | January 28, 2020 |

(Source: Scheme Information Document)

How will HSBC Ultra Short Duration Fund allocate its assets?

Under normal circumstances, the asset allocation pattern will be as under:

Table 2: HUSDF’s Asset Allocation

| Instruments | Normal Allocation (% of Net Assets) | Risk Profile | Debt and Money Market Instruments such that Macaulay duration* of the portfolio is between 3 months to 6 months | Up to 100% | Low to Medium |

*The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the cash flow by the price.

If the Scheme decides to invest in securitised debt, it is the intention of the Investment Manager that such investments will not normally exceed 30% of the corpus of the Scheme. No investments shall be made in foreign securitized debt.

The Scheme shall under normal circumstances not have exposure of more than 50% of its net assets in derivative instruments (including Interest Rate Swaps, Interest Rate Forwards, Interest Rate Futures, Forward Rate Agreements and any such other derivative instruments permitted by SEBI/RBI from time to time). Investments in derivatives would be in accordance with the SEBI Regulations. The cumulative gross exposure through debt & money market instruments and derivative positions shall not exceed 100% of the net assets of the Scheme. The Scheme may participate in securities lending as permitted under the Regulations.

(Source: Scheme Information Document)

What will be the Investment Strategy?

The Macaulay duration of the portfolio will be 3-6 months and within this range the duration management would be largely dependent on the fund manager and his team view rates, yield curve, liquidity, etc.

Given the 3-6 months portfolio duration requirement, the HSBC Ultra Short Duration Fund would have substantial exposure to money market instruments such as Bank Certificates of Deposit (CDs) and Commercial Papers (CPs).

The scheme would largely maintain high credit quality portfolio of securities with investment predominantly in securities that have highest short-term credit quality rating.

The security selection would be driven by investment team’s view credit spreads, liquidity and the risk reward assessment of each security.

For fixed income derivatives the fund manager and his team would do as follows in order to mitigate the risk of debt investments…

- Bond – Swap

- Receive Overnight Indexed Swap (OIS)

- Curve Steepener

- Curve Flattener

Who will manage the HSBC Ultra Short Duration Fund?

The HSBC Ultra Short Duration Fund will be managed by Mr Kapil Punjabi.

Mr Punjabi has completed the Vice President & Fund Manager – Fixed Income at HSBC Asset Management (India) Private Limited and has more than twelve years of experience in research and fixed income management.

He has done his graduation (BMS) and post-graduation (MMS) in management studies from Mumbai University. Before joining HSBC AMC, he was a Fund Manager of Fixed Income at Taurus Asset Management Company Limited and Edelweiss Asset Management Limited.

Prior to that, at Edelweiss Securities Limited he was an Investment Manager and at Trans Market Group Research (India) Private Limited he worked as Research Analyst and Proprietary Trader.

Some schemes which he manages at the Fund house include, HSBC Equity Hybrid Fund(debt portion), HSBC Regular Savings Fund (debt portion), HSBC Debt Fund, HSBC Short Duration Fund, HSBC Cash Fund, HSBC Low Duration Fund, HSBC Flexi Debt Fund, HSBC Overnight Fund and HSBC Fixed Term Series – FTS 130 to 137, 139 and 140.

Table 3: Performance of the schemes managed by Mr Kapil Punjabi

| Scheme Name | Benchmark Name | Managing Since | Scheme Return (%) | Benchmark Return (%) |

| HSBC Cash Fund | Crisil Liquid Fund Index | Dec-2016 | 6.97 | 7.01 |

| HSBC Low Duration Fund | Crisil 1 Yr T-Bill Index | 4.17 | 6.75 | |

| HSBC Short Duration Fund | Crisil Short Term Bond Fund Index | 4.36 | 7.43 | |

| HSBC Flexi Debt Fund | Crisil Composite Bond Fund Index | Feb-2019 | 10.24 | 10.39 |

| HSBC Debt Fund | 9.94 |

(Performance data as on January 15, 2020)

(Source: ACE MF)

As can be seen, the returns of the schemes managed Mr Kapil Punjabi has been in line with the respective benchmark, hence the management style is modest.

The outlook for HSCBC Ultra Short Duration Fund

With the intent to achieve the investment objective, fund manager of the HSBC Ultra Short Duration Scheme will actively manage the scheme and invest accordingly in debt and money market instruments.

As per the product deck, the portfolio construction will be positioned for 3-6 months with respect to yield curve and cites the reasons for it …

- Money market rates are seasonable in nature.

- Rates tend to move up during every quarter-end and drop-in subsequent month to quarter-end.

- Aim to capitalise on the opportunity by positioning in asset maturing beyond March quarter.

- Significant spread is expected among assets maturing between pre-March and post-March months.

- The Yield curve tends to normalise post-March month.

- In the month of January, the fund aims to invest in securities to tap the higher end of defined Macaulay duration band.

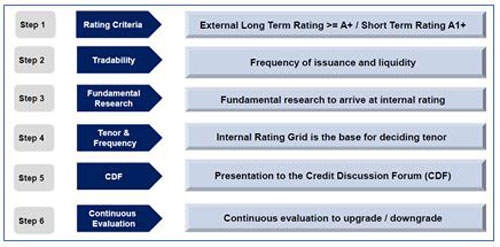

And the guiding principle while construction of portfolio will be the credit quality, securities with high credit quality and liquidity will be chosen to reduce risk.

Image : Strong quality credit research process while portfolio construction

(Source: HSBC Ultra Short Duration Fund Product deck)

The major players in the Indian debt markets today are banks, financial institutions, insurance companies and mutual funds. The instruments in the market can be broadly categorised as those issued by corporates, banks, financial institutions and those issued by state / central governments. The risks associated with any investment are – credit risk, interest rate risk and liquidity risk

In India, RBI operates both as the monetary authority and the debt manager to the government. In its role as a monetary authority, the RBI participates in the money market through open-market operations as well as through Liquidity Adjustment Facility (LAF) to regulate the money supply.

As per the recent data points of the economy, especially pertaining to inflation it has moved up from RBI’s comfort zone. In the year 2019, the RBI cumulatively reduced policy rates by 135 bps in 2019 to support growth. In effect, borrowing rates too came down signalling better transmission yet inadequate.

The 10-yr G-Sec yield inched up marginally by +9 bps in the month of December 2019 and in the year 2019 eased by good -82bps, pursuant to successive policy repo rate cuts by RBI (135 bps since February 2019) and the accommodative stance adopted since the 2nd bi-monthly monetary policy statement for 2019-20 held in June 2019.

Hence, at the outset we seem to have bottomed out with regards to the rate cut cycle, and thus investing at the longer end of the yield curve could prove less rewarding and risky (may encounter high volatility) in the foreseeable future. Most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing policy rates. It reduces the scope of further reduction in policy rates by the RBI to accommodate growth concerns.

Hence, it’s crucial to see how a fund manager will assess these aspects during portfolio construction. Thus, the fortune of HUSDF will be hinged on the quality of paper of money market instruments and debt securities held in its portfolio.

[Read: Skip NFOs, Instead Consider Building A Strategic Mutual Fund Portfolio]

This article first appeared on PersonalFN here

{kind=link}