Investors are being extra cautious in terms of investment, because of sluggish growth, benign inflation and onslaught of successive rate cuts, when the supposedly considered safe debt instrument investments too turned out to be big delusions because of the deepening credit crisis. Investors looking for options that would provide decent returns with low risk preferred Banking & PSU debt funds.

A banking and PSU funds are a category of debt mutual fund that has emerged after the SEBI’s recategorization norms that will invest a minimum 80% of its assets in debt instruments of banks, PSUs, and PFIs.

Usually, this type of fund invests primarily in the bank certificate of deposits or bonds and debentures of public entities that are ‘AAA’ rated, are comparatively less risky than bonds which are AA rated. And are good investment options, as market-related volatility is relatively lower than long-duration funds.

Tata Mutual Fund has launched an open-ended debt scheme, Tata Banking & PSU Debt Fund. It will predominantly invest in debt instruments of Banks, Public Sector Undertakings, Public Financial Institutions and Municipal Bonds to generate income while maintaining the optimum balance of yield, safety and liquidity.

As the fund house is of the view that:

- Strong private banks have solid capitalisation as well as the ability to raise further resources

- For PSUs, credit strength comes from government shareholding and regular support

- Debt instruments issued by these companies have very low credit risk compared to other issuer categories

Hence, instruments issued by Banks and PSUs maintain a decent spread over G-secs and are impacted by Banking System Liquidity & Repo rates. So, Tata Banking & PSU Debt Fund was launched with an aim to minimize credit risk while generating returns through a blend of accruals and rate movements for a short to medium duration of investment, i.e. 3 to 5 years.

Table 1: Details of Tata Banking & PSU Debt Fund

| Type | An open-ended debt scheme predominantly investing in debt instruments of Banks, Public Sector Undertakings, Public Financial Institutions and Municipal Bonds. | Category | Banking & PSU Fund |

| Investment Objective | To generate reasonable income, with low risk and high level of liquidity from a portfolio of predominantly debt & money market securities issued by Banks, Public Sector Undertakings (PSUs), Public Financial Institutions (PFIs) and Municipal Bonds.

However, there is no assurance or guarantee that the investment objective of the Scheme will be achieved. The scheme does not assure or guarantee any returns. |

||

| Min. Investment | Rs 5000 and in multiples of Re 1 thereafter | Face Value | Rs 10 per unit |

| Plans |

|

Options |

|

| Entry Load | Nil | Exit Load | Nil |

| Fund Manager | Mr Amit Somani | Benchmark Index | CRISIL Banking and PSU Debt Index |

| Issue Opens: | 19 September, 2019 | Issue Closes: | 03 October, 2019 |

(Source :Scheme Information Document)

How will the scheme allocate its assets?

Under normal circumstances, the scheme’s asset allocation will be as under:

Table 2: TBPDF’s Asset Allocation

| Instruments | Indicative Allocation (% of net assets) | Risk Profile

(High/ Medium/ Low) |

||

| Minimum | Maximum | |||

| Debt* & Money Market Instruments^ issued by Banks, Public Financial Institutions (PFIs), Public Sector Undertakings (PSUs) and Municipal Bonds. | 80 | 100 | Low to Medium | |

| Debt (including government securities) and Money Market Instruments issued by entities other than Banks, PFIs and PSUs. | 0 | 20 | Low to Medium | |

| Units of REITs and InvITs # | 0 | 10 | Low to Medium | |

^Includes Tri-Party Repo on Clearing Corporation of India (CCIL) platform or any other approved platform.

The net notional exposure (including long and short portion except hedge position) to derivatives will not exceed 50% of the net assets of the scheme.

The cumulative gross exposure through debt, REITs/InvITs and derivative positions should not exceed 100% of the net assets of the Scheme in accordance with SEBI Cir/IMD/DF/11/2010 dated August 18, 2010.

The Scheme will comply with all the applicable circulars issued by SEBI as regard to derivatives viz. SEBI Circular no. SEBI/MFD/CIR No. 03/ 158 /03 dated June 10, 2003, no. DNPD/Cir-29/2005 dated September 14, 2005, no. SEBI/IMD/CIR No. 9/108562/07 dated November 16, 2007, no. Cir/ IMD/ DF/ 11/ 2010 dated August 18, 2010 & SEBI/HO/IMD/DF2/CIR/P/2017/109 dated September 27,2017.

Not more than 25% of the net assets of the scheme shall be deployed in securities lending. The Scheme would limit its exposure, with regards to securities lending, for a single intermediary, to the extent of 5%of the total net assets of the scheme at the time of lending.

The Scheme may participate in repo in corporate debt securities.

The Scheme shall not engage in Short Selling of securities.

# A mutual fund may invest in the units of REITs and InvITs subject to the following:

- No mutual fund under all its schemes shall own more than 10% of units issued by a single issuer of REIT and InvIT; and

- The scheme shall not invest –

- more than 10% of its NAV in the units of REIT and InvIT; and

- more than 5% of its NAV in the units of REIT and InvIT issued by a single issuer.

What will be the Investment Strategy?

The Tata Banking & PSU Debt Fund would seek to invest at least 80% of the portfolio in debt and money market instruments of Banks, Public Sector Undertakings, Public Financial Institutions with the intent of generating reasonable income and at the same time ensuring reasonable liquidity.

The scheme will follow an active investment strategy within the overall mandate, depending on opportunities available at various points in time. Investment in debt & money market instruments issued by Banks, PFIs, PSUs, Treasury Bills & Government Securities is primarily with the intention of maintaining high credit quality & liquidity.

The fund manager will invest in those debt securities that are rated investment grade by credit rating agencies or in unrated debt securities, which the fund manager believes to be of equivalent quality. In-house research done by the fund manager and his team will emphasize on credit analysis, in order to determine credit risk.

Public Financial Institutions shall mean public financial institutions as defined under Section 2(72) of the Companies Act, 2013 and other applicable provisions of the Companies Act, 2013, read with applicable rules/notifications/amendments (including any statutory modification(s) or re-enactment thereof.

Public Sector Undertaking (PSU) means a company in which more than fifty per cent of the paid-up share capital is held by either the Central Government, or by any State Government(s) or partly by the Central Government and partly by one or more State Governments and includes a company which is a subsidiary of a Government company as thus defined.

A PSU is a company in which the Central Government or one or more State Government(s) either singly or together, exercise control over management or exercise power to appoint a majority of directors.

Who will manage the Tata Banking & PSU Debt Fund?

Mr Amit Somani shall be managing the Tata Banking & PSU Debt Fund. He has done his B. Com, PGDBM and is also a CFA Charterholder. He has over 17 years of experience in Global and Indian financial markets specializing in Credit Analysis and Fund Management.

Mr Amit Somani joined Tata Asset Management Ltd. as a Credit Analyst in June 2010 and since September 2012, he has been working as a Fund Manager (Fixed Income).

Prior to joining Tata Asset Management, he has served stints with Fidelity Investments and Netscribes Pvt. Ltd as a Research Analyst and with SPA Capital and Khandwala Securities as a debt market dealer.

Currently, at Tata Mutua Fund, Mr Amit Somani manages Tata Money Market Fund, Tata Liquid Fund and Tata Corporate Bond Fund as the lead fund manager.

Table 3: How have the schemes managed by Mr Somani faired?

| Scheme Name | Benchmark name | Managing Since | Scheme Returns (%) | Benchmark Returns (%) |

| Tata Liquid Fund | Crisil Liquid Fund Index | Nov-13 | 7.83 | 7.77 |

| Tata Money Market Fund | Crisil 1 Yr T-Bill Index | Dec-13 | 6.64 | 7.43 |

| Tata Corp Bond Fund | Crisil Composite Bond Fund Index | May-14 | -3.23 | 7.60 |

(Source: ACE MF, PersonalFN Research)

(Data as on September 23, 2019)

It is evident from the above performance table that except Tata Liquid Fund, the other two debt funds have been underperforming and lagging far behind the respective benchmarks. Hence, it doesn’t exude much confidence to the investors.

The outlook for Tata Banking & PSU Debt Fund

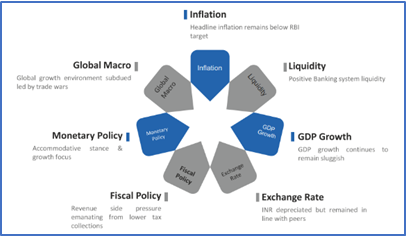

Interest rate basically drives the economy and help in understanding its development. And current factors of sluggish growth, depreciating rupee, and benign inflation has enabled the RBI to take many monetary reforms— further 35 basis point rate cut in the third bi-monthly monetary policy, along with maintaining of accommodative stance and liquidity infusions through OMOs & forex swaps to keep banking system liquidity in surplus in line with RBI’s aim to transmit rate cuts to bank lending rates, to name a few.

Image 1: Variables influencing the interest rate.

Source: (Tata Banking & PSU Debt Fund Presentation)

As mentioned in the presentation, after a long period of maintaining deficit liquidity, RBI has shifted stance to surplus liquidity in the system and this RBI’s focus to maintain surplus liquidity is likely to result in spread compression, presenting alpha generation opportunity for debt funds.

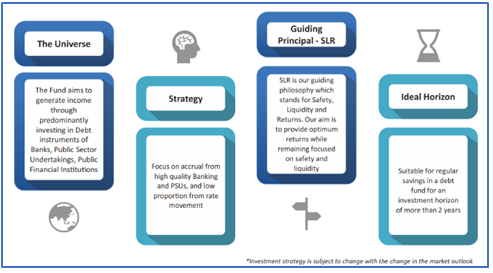

And Tata Banking & PSU debt fund aims to maintain a decent spread over G-secs. Hence, there is low credit risk and is ideal for following a low-risk accrual strategy.

Image 2: Tata Banking & PSU Debt Fund’s proposed approach

Source: (Tata Banking & PSU Debt Fund Presentation)

But the main risks with investments in debt securities are interest rate risk, credit risk and liquidity risk. Interest rate risk associated with debt instruments depends on the macroeconomic environment. It includes both market price changes due to change in yields as well as coupon reinvestment rate risk. Corporate papers carry higher liquidity risk as compared to gilts due to the depth of the gilt market.

So, Tata Banking & PSU debt fund may be affected, inter alia, by changes in the market conditions, interest rates, trading volumes, settlement periods and transfer procedure.

{kind=link}