Last week was a blockbuster Friday for the Indian capital markets — particularly the stock markets. The S&P BSE Sensex and Nifty 50, which seemed unmoved by the earlier announcements made by Ms Nirmala Sitharaman, clocked the highest one-day gains in a decade after Ms Sitharaman slashed corporate tax rates (see table below).

Table: Corporate tax rates cut across categories

| Particulars | Tax Rate (%) Exclusive of surcharge & cess | Tax Rate (%) Inclusive of surcharge & cess | ||

| Old | New | Old | New | |

| For companies with a turnover below Rs 400 crore | 25 | 22^ | 29.12 | 25.17^ |

| For companies with a turnover of over Rs 400 crore | 30 | 22^ | 34.93 | 25.17^ |

| New manufacturing companies* | 25 | 15 | 29.12 | 17.01 |

*Domestic company incorporated on or after 1st October 2019 making fresh investment in manufacturing.

This benefit is available to companies which do not avail any exemption/incentive and commences their production on or before 31st March 2023.

^subject to the condition that they will not avail any exemption/incentive. Also, such companies shall not be required to pay Minimum Alternate Tax.

(Source: Ministry of Finance Press Release)

This move is perceived to be a very positive and bold move to resuscitate India’s shrivelling economic growth, addressing the concerns of consumption slow-down, waning investments, and poor capacity utilization. It has opened the doors for the bulls.

The industry captains hailed the move, with some describing it as:

Big bang reform;

Big reset and will revive the animal spirits in corporate India;

Kick-start the next big economic up-cycle as it will revive the consumption story;

A much-needed gust of fresh air to resurrect and pump prime the economy; and

Demonstrates the government’s ability to come up with big solutions to big problems;

In order to stabilise the flow of funds into the capital market, the press release stated, an enhanced surcharge [introduced by the Finance (No.2) Act, 2019] shall not apply on capital gains arising on sale of equity share in a company or a unit of an equity-oriented mutual fund or a unit of a business trust liable for securities transaction tax, in the hands of an individual, HUF (Hindu Undivided Family), AOP (Association of Persons), BOI (Body of Individuals), and AJP (Artificial Juridical Person).

Well, all that is fine and even true from the industry standpoint – that it will unleash animal spirits and reinvigorate growth.

But what about India’s fiscal deficit and the impact on the debt market?

The recent fiscal measure, estimated to cause a revenue loss of Rs 1.45 lakh, as per the Finance Ministry, will in effect result in compromising on the path to fiscal consolidation charted by the government.

While the fiscal deficit target is set at 3.3% of the GDP (a budgeted fiscal deficit in absolute terms of Rs 7.03 lakh crore) in Ms Sitharaman’s maiden budget, it could likely breach the target by 0.70-0.75 basis points on the upside — even after accounting RBI’s surplus transfer worth Rs 1.76 lakh crore.

Ms Sitharaman at her residence in New Delhi told reporters on Sunday that the government is not revising the fiscal deficit target for now nor cutting spending.

“At this point of time, we are not revising any target. The decision will be taken later.” – Nirmala Sitharaman

India’s fiscal deficit, in the first four months of the fiscal year 2019-20 has crossed 77% of the budgeted estimate of Rs 7.03 lakh crore.

A challenge in accomplishing the fiscal deficit target is the tax collections. India’s tax-to-GDP ratio is around 11%, one of the lowest in the world. While Ms Sitharaman is confident that tax collection target for this year will be met “without any harassment to taxpayers” [as what she mentioned to the press], the fact is that the economic slowdown and high unemployment rate have taken a toll on both, direct tax collection and GST.

Although slashing corporate tax rate would be abetting, it will help draw in tax revenue only from those corporates who are efficiently making profits.

The international rating agency, Standard & Poor (S&P) has viewed the move of slashing corporate tax rate as a “credit negative development” as it expects the fiscal deficit to widen, although potentially boost the broader economy.

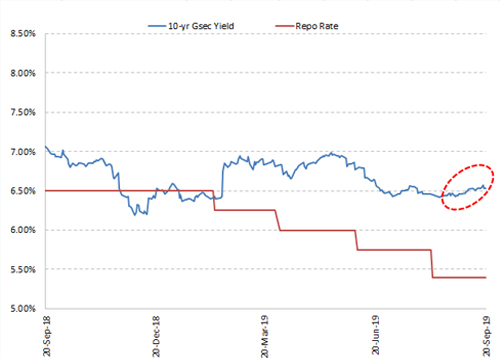

Graph: The Indian debt market has reacted adversely…

Data as of September 20, 2019

(Source: RBI)

The 10-year G-sec yield hardened by good 15 bps on Friday, September 20, 2019, after the corporate tax rate cut announcement.

Besides, factors such as, international oil prices heating up (after Iran’s drone strike on Saudi Arabia’s Aramco refinery triggered supply concerns), possibility of a higher import bill, risk imported inflation, possibility of higher trade deficit amidst a weak Indian rupee, among many others have already upset the Indian debt market resulting in a higher risk premium. The benchmark yield has gradually moved up in the last one month.

The RBI Governor, Mr Shaktikanta Das, at Bloomberg India Economic Forum a day earlier (on Thursday), September 19, 2019, stated: “If you look at government borrowing together with public sector borrowing, there is little fiscal space.” He even went on to add, “There is little space for any fiscal expansion. It is important to do policy changes, focusing on ease of doing business, and structural reforms.”

However, after Ms Sitharaman slashed corporate tax rates on September 20, 2019 (Friday), Mr Das at an India Today event hailed the move:

“These are definitely bold and welcome measures. It will augur extremely well and will be highly positive for the economy,” — Shaktikanta Das

That said, Mr Das also added: “The fiscal tool has to be used not by just expanding the expenditure in an unplanned manner but by focusing more on the quality of the spend …and the positive thing is it is already happening.”

Path to interest rates…

The future course of policy rate actions, according to Mr Das will depend on the incoming data prints (mainly inflation). He also expressed a view that being a developing economy we cannot have very low rates akin to the developed economies.

In 2019 so far, the RBI has reduced policy rates for the fourth consecutive time aggregating to 110 bps.

Going forward as well, if inflation remains with RBI’s comfort zone, it is likely that the RBI will further reduce policy rate cuts given that the slowdown is hurting the economy. This is what many debt fund managers also expect.

In the minutes of the MPC, many members in their statements have cited negative output gaps and the present benign inflation outlook provides headroom for policy action to close this gap. RBI Governor, Mr Shaktikanta Das, stated:

In view of a weakening of domestic growth impulses and unsettled global macroeconomic environment, there is a need to bolster dwindling domestic demand and support investment activity, even as the impact of past three rate cuts is gradually working its way to the real economy. With headline inflation projected to remain within the target over the next one-year horizon, supporting domestic growth by further reducing interest rates needs to be given the utmost priority. Given the current and evolving inflation and growth scenario at this juncture, it can no longer be a business as usual approach. The economy needs a larger push.

This was the reason for the unusual 35 bps policy rate cut in the 3rd bi-monthly monetary policy statement for 2019-20.

Given that RBI has maintained an ‘accommodative monetary policy stance’ since the 2nd bi-monthly monetary policy statement for 2019-20 held in July, it is possible that we may witness another 50 bps reduction in policy rates in this calendar year, i.e. 2019, in a staggered manner.

The investment strategy to devise while investing in debt market now…

(Image source: pixabay.com; photo courtesy: rawpixel)

In my view, we are in the last leg of a rate cut cycle. Most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing rates. Thus, debt mutual funds with exposure to the longer end of the yield curve, i.e. medium-to-long duration funds, long-duration funds, Gilt Funds, and Dynamic Bond Funds have delivered double-digit returns in the last one year.

But going forward, the gain in these categories may be limited. As mentioned earlier, at most we could expect up to 50 bps reduction in policy rates in a staggered manner this calendar year.

So, investing aggressively at the longer end of the yield curve could prove less rewarding and risky (may encounter high volatility) in the foreseeable future. Contrary to RBI’s expectations, if CPI inflation moves up beyond its comfort zone or medium-term inflation target of 4.0%, the scope for a further policy rate cut from RBI reduces.

Hence, in my view, if you wish to take the risk and exposure at the longer end of the yield curve, consider dynamic style debt funds that have the flexibility to move across maturities of debt papers as per the interest rate scenario.

Ideally, you’ll be better off if you deploy your hard-earned money in shorter duration debt mutual funds. But ensure you approach even short-term debt funds with your eyes wide open and pay attention to the portfolio characteristics and quality of the scheme. The fact is that many debt mutual funds across maturity profiles are grappling with downgraded and toxic debt papers which heighten the investment risk.

So, prefer the safety of principal over returns. Stick to debt mutual funds where the fund manager doesn’t chase returns by taking higher credit risk. Further, assess your risk appetite and investment time horizon while investing in debt funds.

Remember, investing in debt funds is not risk-free.

Alternatively, if you prefer to keep your capital safe, prefer fixed deposits.

[Read: Factors to Look At While Investing In Bank FDs]

This article first appeared on PersonalFN here.

{kind=link}