The Association of Mutual Funds in India (AMFI), released its monthly data, some of the figures were encouraging and some showed signs of subdued performance.

Assets Under Management (AUM) as on 31 May 2019, stood at Rs 25,93,560 crore and crossed a landmark of Rs 25 Lakh crore to (almost) touch a new high of Rs 26 Lakh crore.

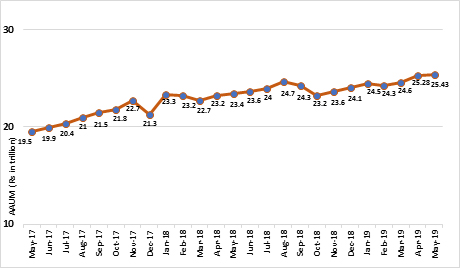

Even the Average Assets Under Management (AAUM) of Indian Mutual Fund Industry for the month of May 2019 stood at Rs 25,43,249 crore.

Graph 1: Average AUM of the Indian Mutual Fund Industry (Rs in Trillion)

Data as of May 31, 2019

(Source: www.amfiindia.com)

The total number of accounts (or folios) as on 31 May 2019, stood at 8.32 crore (83.2 million), while the number of folios under Equity, Hybrid, and Solution Oriented Schemes, wherein the maximum investment is from retail segment stood at 7.51 crore (75.1 million).

Table 1: Monthly rise in No of folios

| Month | No of folios (cr) |

| Mar-19 | 8.25 |

| Apr-19 | 8.27 |

| May-19 | 8.32 |

Data as of May 31, 2019

(Source: www.amfiindia.com)

However, compared to the previous month, there are a lesser number of inflows in debt funds but for equity funds, it has grown by 17%.

Table 2: Monthly inflow/outflow

| Month | Net Equity Inflow | Net debt Inflow |

| Apr-19 | 4,230 | 101,971 |

| May-19 | 4968 | 48,572 |

Data as of May 31, 2019

(Source: www.amfiindia.com)

But in terms of sub-category, Overnight funds, Medium to Long-Duration Funds, Long Duration Funds, and Banking and PSU Funds did witness a good growth.

Table 3: Open-ended Debt fund inflows/outflows

| Open-ended debt Schemes | Net Inflow (+ve)/Outflow (-ve) for the period (in Rs crore) |

Growth (%) |

|

| Apr-19 | May-19 | ||

| Overnight Fund | 95.74 | 2,347.41 | 23.52 |

| Liquid Fund | 89,778.43 | 68,582.91 | (0.24) |

| Ultra-Short Duration Fund | 11,037.26 | 1,190.85 | (0.89) |

| Low Duration Fund | 4,913.30 | -2,353.30 | (1.48) |

| Money Market Fund | 6,418.52 | 3,895.77 | (0.39) |

| Short Duration Fund | 2,770.57 | -1,316.20 | (1.48) |

| Medium Duration Fund | -530.89 | -2,063.18 | 2.89 |

| Medium to Long Duration Fund | 264.14 | 387.21 | 0.47 |

| Long Duration Fund | 8.06 | 90.48 | 10.23 |

| Dynamic Bond Fund | 411.9 | -651.16 | (2.58) |

| Corporate Bond Fund | 3,874.40 | 1,429.98 | (0.63) |

| Credit Risk Fund | -1,253.28 | -4,155.80 | 2.32 |

| Banking and PSU Fund | 2,792.15 | 3,381.82 | 0.21 |

| Gilt Fund | -40.86 | -44.59 | 0.09 |

| Gilt Fund with 10-year constant duration | 33.1 | -61.15 | (2.85) |

| Floater Fund | 347.73 | 232.8 | (0.33) |

| Total | 120920.3 | 70893.85 | (0.41) |

Data as of May 31, 2019

(Source: www.amfiindia.com)

Ever since the IL&FS, DHFL, and Reliance ADAG downgrading crisis, investors began redemptions and heavy outflow of funds was seen for Credit Risk Fund, Low Duration Fund, and Medium Duration Fund. With these three collectively, the bond market witnessed a withdrawal of Rs 8,572.28 crore.

That is because these funds had exposure to a larger portion of ‘AA’ or lower rated papers. Below ‘AA’ rated papers indicate low quality, less capacity to pay interest and repay the principal as compared to ‘AAA’ ratings by the credit rating agencies.

Credit risk fund category had ballooned to make the debt fund stand at Rs 1.4 trillion in assets by September 2018. But now the situation has worsened and there have been increased redemptions; which shows that investors are losing interest to take credit risk and are shying away from it. Slowly even corporate bond funds are turning into under scorers as investors are shifting to higher rated funds like the Banking & PSU funds and overnight funds.

Basically, as per the classification norms of debt funds, they are classified as per the duration of the funds and not the level of credit risk a fund carries. Credit fund and corporate bond funds are the only categories of debt funds which use credit rating.

Whereas ultra-short term, short term funds are free to have been exposed to the risks of any debt instrument if it is identified as risky. This definitely has put several schemes under stressed assets.

Although these low-risk funds are advised/offered to retirees through Systematic Withdrawals Plans, this downgrading spate has led to the risk of concentration as well. And investors bearing the brunt have realised that debt investments isn’t risk-free.

PersonalFN is of the view that the adviser community should educate retail investors and explain with integrity the various underlying risks of any fund. And Investors should ask relevant questions about the risk. In short, cooperation is necessary from both segments to benefit for individual growth in the long run.

[Read: How IFAs Can Gain the Trust and Respect of Their Clients]

{kind=link}